State of Streaming Presents: Attention Capital | A Column by Josh Stein

Editor's Note

Attention Capital is a syndicated column by Josh Stein decoding the economics of media, sports, and platform ecosystems — where attention becomes enterprise value and the contracts behind the cash flow get priced like the credit they actually are. This is Part One of a two-part series on TKO Group Holdings. Part Two publishes tomorrow. Subscribe to State of Streaming to get it in your inbox.

WWE spent a decade trying to become Netflix. Then it stopped.

What TKO built in the 24 months that followed is the cleanest working prototype of live-attention IP as a credit-grade asset class anyone has produced. Four counterparties. Four contracts. One audience class. Roughly $2.2 billion in annual coupons. No customer service organization on the IP owner’s balance sheet. The market read this as media rights. It looks more like infrastructure.

In The Sports Bond, we argued that $300 billion in committed league media rights through 2033 belongs on credit desks rather than media spend lines. In How Lionsgate Won the Streaming Wars by Not Playing, we read a pure-play IP owner as the credit story the streaming wars never wrote. In The Behavioral Bid, a behavioral data system priced a content library and walked away with $82.7 billion. League rights. Pure-play IP. Behavioral pricing. Three pieces of one machine.

The machine has a working prototype. It is publicly traded under the ticker TKO.

For the Attention-Constrained

The asset: Live combat and sports entertainment audiences inside the TKO portfolio. WWE Raw, WWE SmackDown, WWE Premium Live Events, and the full UFC programming engine. Raw alone draws roughly 1.5 to 2 million weekly US live viewers. WrestleMania 40 in April 2024 generated a two-night gate of approximately $38.5 million, the largest in company history at the time.

The platform: TKO Group Holdings (NYSE: TKO). The April 2023 merger of WWE and the Endeavor-owned UFC. Trading began on September 12, 2023, at a combined enterprise value of approximately $21.4 billion. Endeavor took 51%. WWE legacy shareholders kept 49%. Ari Emanuel chairs. Mark Shapiro presidents.

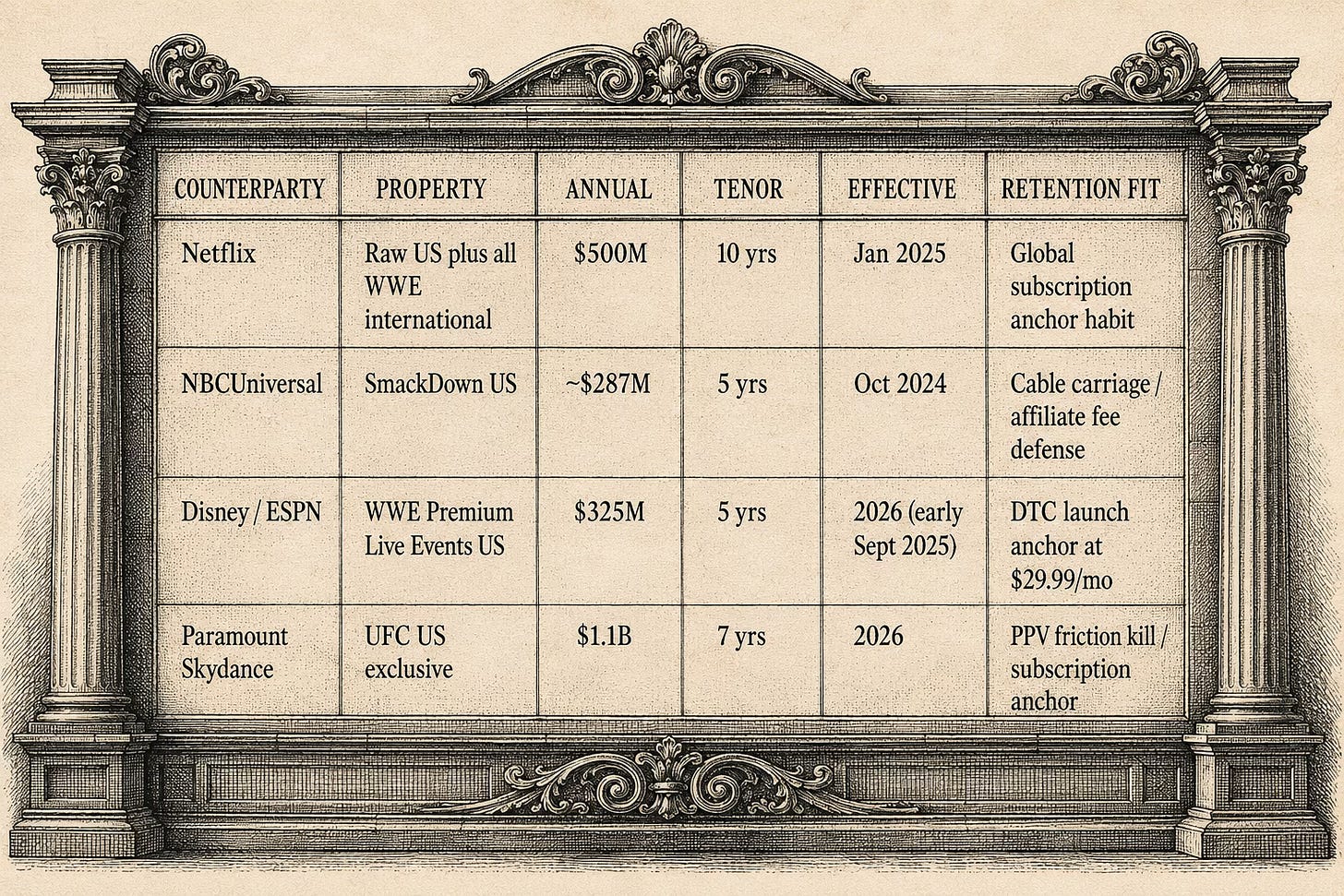

The trade: Four rights deals across four counterparties in 24 months.

Combined annual coupon: roughly $2.2 billion. Combined contracted forward value: north of $16 billion.

The cap table: Silver Lake closed the $25 billion take-private of Endeavor at $27.50 per share on March 24, 2025, the largest private equity sponsor public-to-private transaction in media and entertainment history. Co-investors: Mubadala, Michael Dell’s DFO Management, Lexington Partners, Goldman Sachs Asset Management, and CPP Investments. The public market would not price the asset correctly. Institutional capital took it private to fix the price.

The credit infrastructure: Apollo launched Apollo Sports Capital on September 29, 2025, with Al Tylis as CEO, building on roughly $17 billion in sports capital already deployed across the firm. Apollo’s firm-wide AUM was $840 billion as of June 30, 2025. The new platform targets credit and hybrid exposure across franchises, leagues, venues, media, and events. TKO’s $2.2 billion annual rights stream sits directly inside that mandate.

If you allocate to credit or own live IP, this is the cleanest working example of how to turn one audience into four investment-grade-equivalent coupons without ever touching DTC margin drag.

The Wrong-Fit DTC Trap

WWE Network launched on February 24, 2014, at $9.99 per month. It was the most aggressive DTC bet any IP owner had taken in live entertainment to that point. The pitch was clean. WWE owned the largest video library in sports entertainment, the most consistent monthly live event slate in cable, and a fan base trained for 30 years to pay monthly for premium live programming. Trade pay-per-view margin for subscription volume. Breakeven sat at around 1 million subscribers. WWE crossed that inside a year.

The service averaged roughly 1.65 million paid subscribers in 2018, peaked at around 2.1 million following WrestleMania 34, then plateaued. The wrestling audience was loyal but not infinite. International expansion did not scale at the rate the DTC model needed. The unit economics turned negative once the cost stack loaded against the line: content production for the service, customer acquisition, billing and payments infrastructure, customer service organization, churn management, and the marketing burden of keeping the line growing.

WWE was running a media company and a payments company simultaneously. The payments company was eating into the media company’s margins.

The wind-down arrived in January 2021. WWE licensed the service to Peacock for roughly $1 billion across five years. NBCUniversal absorbed the subscriber base, the billing system, the churn problem, and the marketing burden. WWE retained the content, the events, the IP rights, and the cash. The decision converted the company from a DTC operator with negative-margin overhead into a pure-play licensor with a credit-grade counterparty paying a flat annual coupon. The numbers got cleaner the same day.

This is the lesson Disney has spent five years and over $10 billion in cumulative DTC losses learning. It is the lesson Warner Bros. Discovery confirmed in Q2 2024 with a $9.1 billion linear-network impairment. It is the lesson Paramount, carrying roughly $14.5 billion in long-term debt against a declining linear cash flow base, is still processing under new ownership.

TKO has not made the mistake again. There is no TKO Network. There is no UFC subscription product owned by TKO. There is no Premium Live Events DTC service rebuilt under a new brand. The IP owner stayed on the IP side and sent every audience slice to a platform that already owned the cost stack for that slice.

The Peacock-WWE deal expires in March 2026. The replacement was not a relaunched WWE Network. The replacement was four deals with four counterparties, each structured around the retention model required by that counterparty.

The payments company was eating the margin that the media company was producing.

The Netflix Raw Trade

On January 23, 2024, Netflix and WWE announced a 10-year, $5 billion exclusive deal for Monday Night Raw, effective January 2025, with international scope covering all WWE programming, including SmackDown, NXT, and Premium Live Events. The structure includes a Netflix option to extend for an additional 10 years, with an opt-out after the initial five.

$500 million per year. Ten-year tenor. Counterparty is Netflix.

This is the textbook instrument-asset-fit case. Netflix owns the most efficient subscriber retention machine in entertainment, sitting on 301.6 million paid memberships globally as of Q4 2024 and a content library priced against churn math measured to the basis point. S&P upgraded Netflix to an A credit rating in July 2024. Operating cash flow exceeds $8 billion annually. The counterparty risk on the $500 million annual coupon is the credit risk of an A-rated public company.

Netflix needed live programming for one specific operational reason. Appointment viewing within a streaming bundle resists the most common churn pattern: the lapsed casual subscriber who opens the app only when a specific show is in season. WWE Raw runs 52 weeks a year on Monday nights. The audience does not break for a hiatus. The audience does not wait for a renewal announcement. Plug that into a streaming subscription, and you have inserted an anchor habit into a bundle whose largest churn vulnerability is the lack of one.

Netflix took on platform-side risk: subscriber acquisition costs against the new audience, the build for advertising integration, technical infrastructure for global live concurrency, and the operational learning curve of weekly live broadcasting at scale. WWE took none of it. WWE collected the coupon and kept the IP.

The IP owner controlled the framing of the asset to the platform. TKO President Mark Shapiro later described the pitch to Netflix directly:

“It’s up your alley. Why don’t you dip your toe in? It’s not really live sports. It’s scripted entertainment. Very serial in nature. Every single week."

Shapiro sold Netflix on the retention model fit, not the live sports premium. The pitch reframed the asset to align with the buyer’s subscriber-retention math. The premium Netflix paid was for what Sarandos called “the drama of sport,” running 52 weeks a year. Same audience. Same content. Different P&L logic priced against the platform’s actual churn problem.

Read as credit, the deal is a 10-year contracted receivables stream against an A-rated counterparty with a global investment-grade balance sheet. A senior-secured facility against receivables would price tighter than most BB-rated leveraged loans. In plain English: cheaper funding than a typical sub-investment-grade corporate borrower pays.

The deal landed at the moment Vince McMahon was stepping down from TKO’s board on January 26, 2024, amid sexual assault and trafficking allegations. The same week, Dwayne Johnson joined the TKO board with a $30 million-plus stock grant and a service and trademark agreement that transferred full ownership of “The Rock” mark from WWE back to Johnson. The board rotation, the trademark transfer, the Netflix announcement, and the cap table reset all happened inside a 72-hour window. TKO equity priced up materially across the same week and held the print.

What Netflix bought was not Raw. Netflix bought a behavioral anchor that the recommendation engine could not produce on its own. The competition for that anchor was the entire weekly slate of live programming on US cable, none of which Netflix could touch without striking a deal with the rights holder. WWE held the only inventory in that retention category at that price point.

Part Two publishes tomorrow.

How WWE parsed the same audience four ways across SmackDown, WrestleMania, and the UFC. Why Silver Lake took Endeavor private rather than let the public market price it. What Dwayne Johnson's board seat actually is. And the one thing still missing from the architecture.

Subscribe to State of Streaming to get Part Two in your inbox.

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.