The Great Auto Ad Reset: Why First-Party Data Is the Only Playbook That Survives a Contracting Market

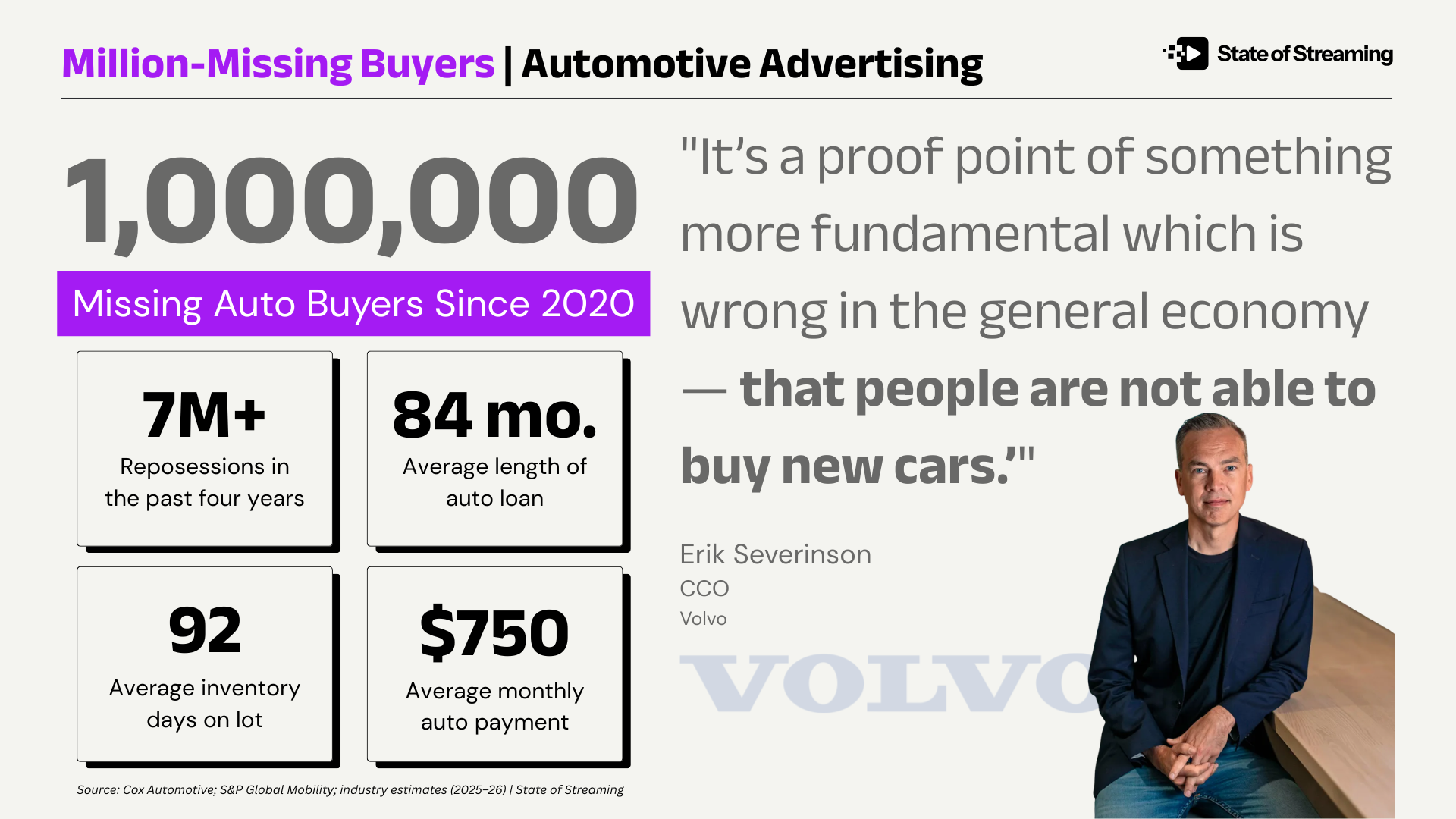

The U.S. auto industry is staring at a number it can't explain away. One million prospective new-car buyers have left the market since 2020. GM, Ford, and Toyota are planning for sales to stagnate or shrink.

Volvo's CCO Erik Severinson put it bluntly —

‘It’s a proof point of something more fundamental which is wrong in the general economy—that people are not able to buy new cars.’”

The instinct across the industry — at OEMs, at agencies, at dealer groups — will be to pull back. Cut budgets. Wait for rates to drop. Hope the buyers come back.

But it's the wrong call, here's why:

The Market Didn't Disappear. It Got Harder to Read.

Brian Maygra put it plainly on LinkedIn:

"The average monthly car payment for a new car is over $750 a month. People aren't going to buy new cars if they can't put food on the table."

He's right on the economics. But inside every contracting market, there are still buyers. They're just harder to find and more expensive to lose.

Craig Faunce named the product problem underneath the price problem: "Car payments are now exceeding what I paid in rent in my 20s. Oh, and they're full of LCD screens and software that nobody really wanted."

Vince Luppino, a retired Toyota training specialist — someone who spent a career inside the industry — said the same thing from the other side of the counter:

"If the industry starts to build real cars, not rolling computers, and prices them so people can afford them, the industry will sell."

These aren't just social media comments. They're data points. They're telling you exactly what a hesitant buyer sounds like, what objections live between your ad impression and a showroom visit, and what would have to be true for them to convert.

And so the question isn't whether to advertise into a shrinking market. The question becomes whether you know who you're advertising to...and why.

The Repossession Spiral

The WSJ's "one million missing buyers" headline is actually the conservative number. The structural exclusion runs much deeper.

In 2023, approximately 1.5 million Americans had their vehicles repossessed. In 2024, that number rose slightly to an estimated 1.73 million. While repossession figures for 2025 and 2026 remain elevated due to high auto loan delinquency rates, industry projections track lower than initial fears, stabilizing closer to 1.8 to 2.2 million annually.

Combined, this results in roughly 7 million repossession events over four years. Each event represents a household facing severe credit damage, effectively locking them out of the new car market for several years while their credit recovers.

From there, the repo spiral compounds in ways the headline number doesn't capture.

Used car prices are up 6.2% year-over-year precisely because repo'd buyers flood the used market, driving up demand there too. And the used market trap is worse than it looks: average used car loan rates run 11-12% nationally, compared to 6-7% on new. For buyers with damaged credit, rates reach 15-22%. The scenario becomes "save $10,000 on the sticker and pay it back twice over in interest." The math punishes the exact buyers who can least afford it.

Meanwhile, 92 days of new vehicle supply sits on lots nationally — well above the healthy 55-60 day benchmark. Some dealers are carrying five-plus months of inventory, which means unsold 2025 units are still sitting in late May 2026, when the industry historically clears prior-year stock by mid-April. The inventory crisis is telling OEMs and dealers something they don't want to hear: price is not the only factor for the buyers who are left.

Did You Know?

Over 23% of all new car loans taken out in 2025 were 84-month terms.

The average new car loan duration is now 69 months.

Those households aren't in-market for another vehicle for five to seven years.

The Passion Buyer Is Tapping Out Too

The signal isn't only coming from dealership lots. The collector car market — long a proxy for how deeply Americans are emotionally invested in cars as a category — is showing the same fracture lines.

Hagerty's Market Index has fallen roughly 17% from its December 2022 peak.

Mecum Kissimmee 2026 posted sell-through rates around 70%, down from 75% the year prior.

Mecum Indy saw "Bid Goes On" — auction language for failing to meet the reserve minimum — appearing repeatedly across the bread-and-butter muscle car segments that exploded during pandemic-era speculation. The mid-market collector buyer, the enthusiast who bought a Fox Body Mustang or a square-body truck as an appreciating asset, is pulling back too.

Critically, the top of the market holds. Seven-figure Ferraris and ultra-rare exotics still clear. The bifurcation mirrors the new car lot exactly: $105,000 GMC Yukons sit unsold while ultra-premium product finds buyers. The middle is collapsing in both markets simultaneously.

For advertisers, that revaluation changes the creative and targeting brief entirely.

Why Auto Can Be the Category to Get This Right

Here's what the contraction doesn't change: the fundamental unit economics of automotive advertising remain the most compelling in any category.

A CPG brand might spend $8 to acquire a customer worth $200 over three years. An auto dealer is spending thousands to acquire a customer worth $40,000 to $80,000 over a relationship that — managed well — spans multiple vehicles, service revenue, financing, parts, and referrals. The lifetime value math dwarfs almost every other category an ad agency works with.

That asymmetry should change everything about how dealers and OEMs think about media in a contracting market. When lifetime value is that high, the math on first-party data investment is obvious. You can afford to know your customer deeply. You can afford to build audiences from your best buyers and find more people who look like them. You can afford — and frankly can't afford not — to treat every media dollar as both an outcome generator and a data collection instrument.

Every impression, every click, every form fill, every service appointment is a signal that sharpens your model. The brands that figure this out won't be the ones with the biggest budgets. They'll be the ones running the tightest feedback loop between customer data and media activation.

Two Goals. Every Campaign. No Exceptions.

The automotive industry has a habit of overcomplicating its marketing objectives. Brand campaigns, conquest campaigns, retention campaigns, service campaigns — each with its own budget, its own vendor, its own measurement framework, operating in silos that make it nearly impossible to see the customer whole.

Strip it back.

There are only ever two goals:

Get more new customers who look like your best ones.

Keep your best ones coming back.

Everything else — share of voice, brand awareness, market share plays — is an amplifier. It works when the first two are working. It's waste when they aren't.

In a market where buyers are disappearing at multiple points in the funnel — priced out, repo'd out, stretched into 84-month loans they can't exit — the instinct is to yell louder at everyone. The better move is surgical. Who are your best current customers? What does their journey look like from first search to first service appointment? Where did you reach them? What made them convert when the person in the same demographic didn't?

That profile is your most valuable asset. Not your creative. Not your media plan. Your customer data.

Abel Baruwa framed the market moment in two sentences that should be taped to every auto marketing team's wall right now:

"The new car market isn't just slowing down. It's structurally resetting."

A structural reset doesn't reward the brands that wait it out. It rewards the ones that use the contraction to build infrastructure that outperforms when volume returns.

Media as a Data Collection Lever, Not Just a Reach Mechanism

Here's the reframe that changes the economics of auto advertising in this environment:

Every media dollar you spend should be doing two jobs.

The obvious job is generating a near-term outcome — an opportunity for a showroom visit, a test drive booking, a service appointment.

The less obvious job is collecting a signal about who responded, how, and under what conditions.

That second job is how you build the first-party data asset that makes every future campaign more efficient, every conquest audience more precise, every retention play more timely.

Amber Daniel, Chief Revenue Officer at Cognition and a twenty-year veteran of digital automotive advertising, frames the activation gap precisely:

"The strategy is around first-party data — understanding who I should be targeting, who I shouldn't be targeting, and utilizing technology like identity graphs to give yourself a better opportunity to reach those customers on an end platform."

The suppression half of that equation — who you don't target — is where most dealers are leaving money on the table.

Television has always been particularly well-suited to this, the biggest difference with streaming being that household-level targeting has matured to the point where you can close the loop between an ad exposure and a dealership visit. Automotive OEMs and dealers can match a household from the ad they saw to the customer who appeared on your lot.

Dealers who understand this stop asking "what's my cost per lead" and start asking "what's the investment required to add a high-value household to my first-party data asset." Those are different questions with different answers and very different long-term trajectories. The first optimizes for this month. The second builds an asset that compounds.

The 84-month loan data makes this concrete. If you know which households in your market are locked into long-term loans — not in-market for years — you can suppress them from conquest spend and redirect that budget toward the households that are actually qualified. Follow up with those other buckets of customers with messaging relevant to where they are in their lifecycle.

None of this is a sophisticated data science problem. It's a basic audience intelligence question that most dealers aren't asking because they're still activating media like it's 2018.

The Brands That Win the Reset

The million missing buyers will come back. Some of them. In one way or another. Rates will eventually ease. Affordability will shift at the margin. When it does, the brands with clean customer data, tight lookalike audiences, and a media strategy built around outcome loops will capture disproportionate share of the recovery.

The brands that went dark — that treated a contracting market as a reason to pull back — will spend twice as much to reacquire the awareness they abandoned and rebuild the data asset they never built in the first place.

The structural reset is real. But it's not a threat to every player equally.

It's a catastrophe for the ones running volume-era playbooks against a precision-era market. And it's a compounding advantage for the ones who use the contraction to do what the easy years never forced them to do: actually know their customer.

The million missing buyers aren't gone. They're just in someone else's CRM. Your job is to get them into yours.

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.