The Living Room Already Changed Hands (Part One) - Attention Capital | A Column by Josh Stein

Editor's Note

Attention Capital is a syndicated column by Josh Stein decoding the economics of media, sports, and platform ecosystems — where attention becomes enterprise value and the contracts behind the cash flow get priced like the credit they actually are. This is Part One of a two-part series on creator content as a mispriced asset class. Part Two publishes tomorrow. Subscribe to State of Streaming to get it in your inbox.

In March, Spotter staged its second annual Showcase in New York. The pitch to 150 brand marketers: creator content is television now. Buy it like television.

Creator Content is TV

They brought out MrBeast, Dude Perfect, the Try Guys. They coined a term: “Creator TV.” They presented viewing data showing that 76% of their top creators’ audiences watch on living room screens. They showed that 72% watch more than three episodes per session. Binge behavior. Lean-back consumption. The same patterns Netflix optimized for a decade ago.

The applause happened. Then the media buyers went back to their desks and kept treating creator content like a discount tier of premium video.

That’s the gap this piece is about.

The living room already changed hands. YouTube now commands 13.4% of all U.S. television viewing. More than Netflix. More than any cable network. More than any broadcast channel. More than 150 million Americans watch YouTube on connected TVs every month. The platform crossed $60 billion in annual revenue in 2025. Larger than Netflix. Larger than the combined ad revenue of Disney, NBCUniversal, Paramount, and Warner Bros. Discovery.

The content won. The capital hasn’t caught up.

Creator content on living room screens sells at CPMs 60-75% below comparable premium CTV inventory. The financing infrastructure that funds Hollywood production at scale doesn’t exist for creators reaching comparable audiences. The entire ecosystem still operates as if “creator” means “bedroom with a ring light” rather than what it has become: the dominant form of American television.

This piece maps the structural gap between where attention already lives and where capital still refuses to follow. Because when you see the numbers, the mispricing becomes obvious.

Obvious mispricings don’t stay mispriced forever.

For the Attention-Constrained

The audience shift: YouTube accounts for 13.4% of all U.S. TV viewing, according to Nielsen. TV surpassed mobile as YouTube’s primary viewing device in 2025. Long-form content (30+ minutes) accounts for over 70% of YouTube watch time. The living room belongs to creator content.

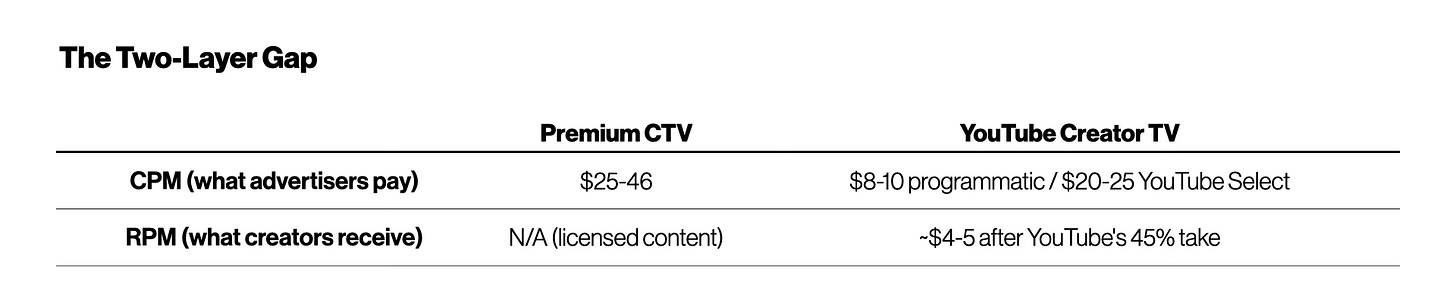

The pricing gap: Netflix commands $31 CPMs. Disney+ charges $46. YouTube creator content on the same living room screens sells for $8-10. That’s a 60-75% discount for content reaching comparable audiences during the same primetime hours. The gap compounds on the sell side: after YouTube’s 45% take, creators net ~$4-5 RPM on inventory advertisers paid $8-10 to reach.

The financing gap: MrBeast spends $3-4 million per vi6deo. Dude Perfect raised $100 million from Highmount Capital. Mark Rober is personally financing a $30 million science curriculum. Traditional TV production has deficit financing, completion bonds, and gap lenders. Creator content has none of it. Spotter and Karat address pieces of the problem. Nobody is doing what Hollywood studios do: advancing production costs against projected future revenue.

The thesis: The market structure for creator content is mispriced against observable audience behavior. The advertising gap will close as measurement improves and generational change hits agencies. The financing gap represents the real opportunity: credit structures built for content that behaves like television but isn’t funded like television.

Why it matters: Whoever builds the production financing infrastructure for creator-scale content is positioned for a market where audience economics and capital economics finally converge.

The Takeover Nobody Announced

Nielsen publishes a monthly report called The Gauge. It measures what Americans actually watch on television. Not surveys. Not panels. Actual viewing behavior across every screen that displays content in a living room.

The data tells a story the industry still hasn’t absorbed.

YouTube first claimed the #1 streaming spot in February 2023. It has held that position for nearly three years in a row. In July 2024, it became the first streaming-only company to surpass Disney’s entire portfolio of broadcast, cable, and streaming properties in total viewing share.

The numbers keep climbing. July 2025: YouTube hit 13.4% of all U.S. television viewing. Its sixth consecutive month as the #1 media distributor. Its lead over #2 Disney (9.4%) was 4.0 percentage points, the largest gap Nielsen has ever recorded between the top two distributors.

That same month, total streaming (44.8%) surpassed combined broadcast and cable for the first time in history.

YouTube CEO Neal Mohan confirmed in February 2025 what the data had been showing for months: TV screens had become the primary device for YouTube viewing in the United States. Not a secondary screen. Not a supplementary device. The primary screen. For more than half of the top 100 most-watched YouTube channels globally, TV is now their most-watched device.

The consumption patterns look like traditional television because they are traditional television. Average YouTube CTV sessions run 45-52 minutes. Primetime peaks between 7 and 11 PM. More than 70% of watch time goes to videos 30 minutes or longer. Viewers watch multiple episodes in sequence. They lean back. They let the algorithm serve the next video.

These aren’t the behaviors of someone scrolling a phone during a commercial break. These are the behaviors of someone who replaced broadcast television with something better.

The living room screen is the ultimate legitimizer. Once content appears on it, the distinction between “professional” and “creator” becomes invisible to the viewer.

The scale is staggering. Google disclosed that viewers worldwide watch over 1 billion hours of YouTube on connected TVs daily. YouTube’s full-year 2025 total revenue crossed $60 billion, larger than Netflix’s $45 billion. Its ad revenue alone exceeded the combined ad haul of Disney, NBCUniversal, Paramount, and Warner Bros. Discovery.

Walk into any media buying meeting. Creator content is still categorized as “social video.” The budgets still flow to the platforms that lost the living room.

What Television-Scale Actually Looks Like

The phrase “creator economy” does a disservice to what’s actually happening. It sounds like side hustles and sponsorship codes. The reality looks more like mid-tier Hollywood.

Dude Perfect raised $100-300 million from Highmount Capital in April 2024. The first outside money the group had taken in 15 years of operation. Consider that for a moment. Five guys from Texas A&M spent a decade and a half building a 60-million-subscriber media company without a single outside investor. The deal implied a valuation between $250 and $400 million.

Revenue had grown from $20 million in 2021 to approximately $50 million in 2024. The company now employs 50 people at its 80,000-square-foot headquarters. Their planned “Dude Perfect Factory” carries a budget over $100 million: 30 acres, three stories, a 330-foot trick-shot tower, a museum, mini-golf, and restaurants.

Coby Cotton told interviewers: “We got offers from every PE firm I could think of, all across the board, including full buyouts.”

RockWater Industries ran the math on what Highmount needs for target returns. The answer: Dude Perfect is reaching roughly $750 million in valuation. Aggressive. But indicative of the scale PE firms now see in creator businesses. These aren’t lifestyle investments. These are growth equity bets on media infrastructure.

Private equity doesn’t chase bedroom operations. They chase scale. They’re finding it on YouTube.

Mythical Entertainment operates from a Burbank studio with approximately 110 employees, producing content seven days a week across channels that total 32 million subscribers and 12 billion lifetime views. Revenue and headcount have more than quadrupled since 2016. The company has never raised external institutional capital for core operations.

Yet it participated in the $82.5 million acquisition of First We Feast (Hot Ones) from BuzzFeed in December 2024. Soros Fund Management led. Sean Evans took an ownership stake. Crooked Media participated. Mythical, a creator company, sat at the table as a strategic acquirer.

Mythical previously acquired Smosh for under $10 million in 2019 when Defy Media collapsed. They grew it. Then sold it back to co-founders in 2023 while retaining a minority stake. Breeze Financial funded the buyback. Post-acquisition, Smosh doubled its employee count to roughly 125 and announced a move from 17,000 to 32,000 square feet of studio space.

That’s roll-up logic applied to YouTube channels. Acquire distressed assets. Professionalize operations. Exit to founders or strategics. Rinse and repeat.

Brian Flanagan, promoted to President in 2024, declared the ambition plainly: “to be the definitive television studio for the internet generation.”

The internet generation already watches more YouTube than cable. Mythical is building the studio system for what comes next.

Mark Rober publishes only 10-11 YouTube videos per year to his 72 million subscribers. Each one involves production at a scale few traditional shows attempt. He sent a satellite to space. Built a goalie robot to compete against Cristiano Ronaldo. Filmed an escape from Alcatraz. His company, CrunchLabs, employs roughly 100 people. He’s personally financing a $30 million free science curriculum for schools.

CrunchLabs’ newly hired Chief Content Officer Scott Lewers, formerly of Warner Bros. Discovery, described the operating reality: “What most YouTubers or creator channels are is a weekly beast. His videos are big. These things are not something you do in six days and shoot on a Sunday.”

The Try Guys provide perhaps the most candid window into the financing pressure. Co-founder Zach Kornfeld told CNBC: “Our company was operating at a loss for essentially two years. We got to a point where it cost more money for us to make the shows our audience loved than we got in from YouTube.”

Their response was radical. In May 2024, they launched 2nd Try TV, a standalone subscription streaming service at roughly $5/month. Within three months, the service accounted for approximately 20% of total company revenue and put the company on track to profitability.

Kornfeld’s diagnosis was blunt: “Having a business that is reliant on ads is very unstable and very unpredictable. It’s tenuous at best. Corrosive and explosive at worst.”

These aren’t hobbyists who got lucky. These are operators building studios without the financial infrastructure that studios have always relied on.

The CPM Canyon

Here’s where the mispricing becomes undeniable.

Netflix launched its ad-supported tier at $60-65 CPMs. That price has eroded as the company chased scale, settling around $31 by early 2025. Still the highest in streaming.

Disney+ commands roughly $46 CPMs. Hulu ranges from $25 to 35. Peacock and Paramount+ both landed around $26 after their 2024 upfronts. Amazon Prime Video launched ads at $30-35 and has since drifted toward $20-25.

YouTube creator content on connected TVs? Strike Social campaign data shows $8.72-$10.01 CPMs through Google Ads. Premium direct buys through YouTube Select run $20-25, competitive with mid-tier streamers but still below Netflix and Disney.

That’s a 60-75% discount for content reaching the same screens, in the same rooms, during the same hours.

The buy-side gap is a CPM story. What creators actually receive is a separate compression. YouTube’s 45% take and programmatic auction dynamics further widen the distance between what advertisers spend and what publishers capture. Two layers of mispricing, not one.

The first layer is buy-side: advertisers paying less for comparable inventory. The second layer is sell-side: creators capturing a fraction of what advertisers actually spend. Operators who control their own ad stack and sell direct can close both gaps simultaneously, commanding premium CPMs while guaranteeing creator RPMs that dwarf programmatic yields.

The market is paying broadcast prices for legacy TV and mobile social prices for the platform Americans now watch most. That’s not a feature of the market. That’s a bug waiting to be corrected.

The explanations are always the same. Brand safety. Measurement fragmentation. Lack of show-level transparency. The user-generated nature of the content library.

One agency executive put it bluntly to Digiday: “It’s been very tough for clients to know contextually or from a genre perspective where their impressions are running.”

Here’s what those explanations miss: the audience already made its choice. The viewers who spend 45 minutes watching a MrBeast video on their TV don’t care whether the buyer offers granular show-level transparency. They’re watching. They’re engaged. They’re in the living room.

The buyers are pricing the content as if it were still mobile social video. The viewers are consuming it as television.

Creator content carries a 60-75% CPM discount on living room screens. The audience doesn’t know that. Neither does the attention.

In Q1 2025, something shifted. YouTube ad spend on CTV screens surpassed mobile for the first time: 43% of YouTube ad placements ran on connected TVs, compared with 42% on mobile. Nearly double the CTV share from a year earlier.

The money is starting to follow. The gap remains.

Samsung, Tubi, and Netflix Are Already Buying

The distribution landscape expanded dramatically in 2025. Three tiers emerged: FAST channels, ad-supported streaming, and premium subscription services. Each represents a new monetization path for creator catalogs.

Samsung TV Plus made the boldest FAST play. The platform expanded from 2 creator channels to more than 10 in July 2025, featuring Mark Rober, Dhar Mann, Smosh, The Try Guys, Michelle Khare, Epic Gardening, Donut Media, and Brave Wilderness. Combined: over 175 million YouTube subscribers.

Samsung struck the first-ever FAST-original creator content deal: 13 original episodes produced by Dhar Mann Studios exclusively for Samsung TV Plus. The platform surpassed 100 million monthly active users globally by January 2026.

Mark Rober’s FAST channel launched across 18 countries in November 2025. His observation: “We found that you generally don’t cannibalize an audience by moving to a different medium.”

That’s the key insight. Creator content has been trapped on a single platform. These distribution deals create a secondary market.

Tubi built a scalable pipeline. The platform launched “Tubi for Creators” in June 2025 with 500 episodes, expanding to nearly 10,000 creator titles by late 2025. They hired Kudzi Chikumbu, TikTok’s former global head of creator marketing, as VP of Creator Partnerships.

A key data point for creators: 31% of Tubi’s audience is not on YouTube. That makes it a genuine audience expansion channel rather than a cannibalizing one.

At the premium tier, Netflix has moved aggressively into creator content. The streamer that once seemed allergic to YouTube talent is now actively farming it.

Ms. Rachel (13 million YouTube subscribers) delivered just 4 exclusive episodes, which became the 7th-most-watched show on Netflix in the first half of 2025, with 162 million hours viewed. Four episodes. 162 million hours. The efficiency ratio is staggering.

Cocomelon, which originated on YouTube and has 193 million subscribers, was the #2 most-watched program on Netflix in 2024, behind only Bridgerton. A children’s channel that started uploading nursery rhymes now outperforms prestige drama.

Mark Rober’s CrunchLabs series hit Netflix’s global top 10 within days of launch. His pipeline now includes “SCHOOLED!,” a competition series co-produced with Jimmy Kimmel’s Kimmelot, announced in March 2026. Netflix described it as a show where “kids compete in explosive science and engineering challenges.”

Jordan and Salish Matter (34 million YouTube subscribers, 13.3 billion lifetime views) signed what Netflix called its “biggest creator deal yet” in February 2026. The scope: scripted, unscripted, animated series, consumer products, and experiential offerings. A multi-format development deal that looks like what Netflix gives established production companies.

The 16-year-old Salish had already launched a skincare line at 384 Sephora stores in September 2025. It sold out within a week. The launch event at American Dream mall drew 87,000 people, reaching capacity by 7 AM. Strand Equity provided seed investment.

Netflix co-CEO Ted Sarandos framed the relationship directly: YouTube is “a little bit of a farm league” where creators “cut their teeth.”

The farm league has more viewers than the majors. But it’s still getting paid like the minors.

Part Two publishes tomorrow.

The audience is in the living room. The distribution deals are signed. Netflix called YouTube the farm league — while the farm league outdraws the majors. Tomorrow: why creator content is still priced like mobile social video, why the production financing infrastructure doesn't exist, and what the credit structure that should already be in market actually looks like.

Subscribe to State of Streaming to get Part Two in your inbox.

Is YouTube The New Prime Time? How Creator-Led Shows Are Dominating Connected TV

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.