Streaming Won. Linear Owes $57 Billion.

Key Takeaways

Streaming turned profitable across every major platform in Q1 2026 — simultaneously — while affiliate and retransmission revenue collapsed at the same companies on the same earnings calls.

Legacy media companies are carrying a combined $57 billion in debt borrowed against linear revenue that no longer exists at the scale it was underwritten; Optimum's $2.7 billion asset write-down is the first formal balance sheet admission of that gap.

Buying linear inventory from debt-distressed sellers is not a value play — it is a liquidity subsidy, and the advertisers who reallocate to streaming infrastructure now will reprice before the rate card catches up to Q1's profitability data.

For thirty years, cable worked like a tollbooth.

Every time a household paid a cable bill, a portion traveled upstream — to Disney, to Warner Bros., to AMC, to Paramount — as a fee for carrying their channels. Those fees funded everything: the studios, the sports rights, the content libraries, and eventually the billions of dollars it cost to build the streaming services that were supposed to replace cable.

Streaming was built with cable's money.

That is the part nobody says out loud. And Q1 2026 is the quarter that arrangement ended. Not gradually either. All at once, across eleven earnings releases filed in the last six weeks.

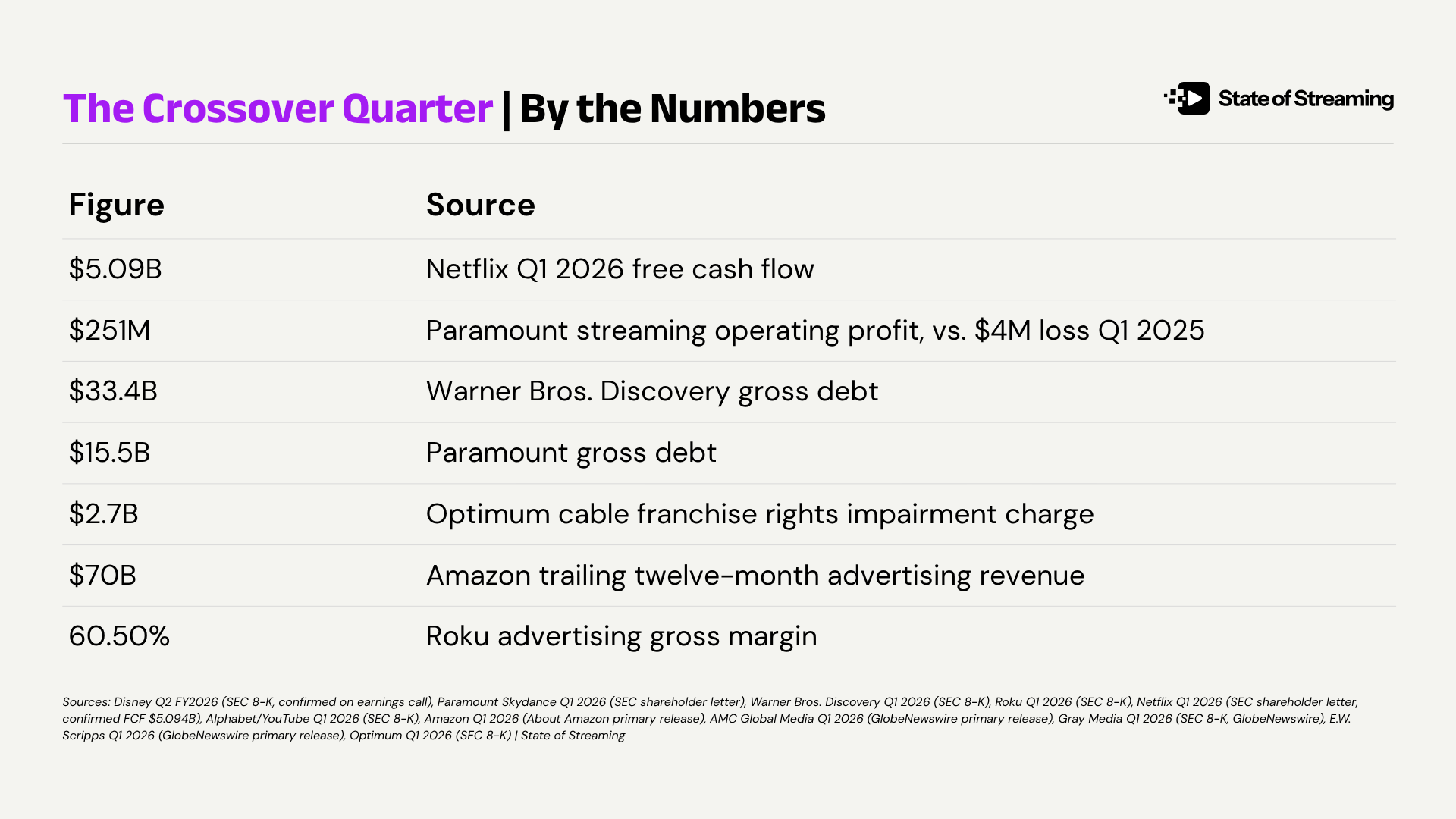

Disney's streaming business generated more than double the revenue of its linear television business for the first time — confirmed in the company's Q2 fiscal 2026 SEC filing and on the earnings call by CFO Hugh Johnston. Paramount's streaming operation swung from a $4 million operating loss to $251 million in operating profit in twelve months. Warner Bros. Discovery's streaming operating profit grew 29%. Peacock crossed $2 billion in quarterly revenue for the first time. Netflix generated $5.09 billion in free cash flow in a single quarter — a figure that includes a $2.8 billion one-time cash receipt from the Warner Bros. transaction termination fee, but cash flow is cash flow.

The cable side filed the opposite result.

AMC's affiliate revenue — the tollbooth fees cable pays to carry channels — fell 16%. Gray Media retransmission consent revenue dropped 11%. Paramount affiliate revenue declined 6%. Warner Bros. Discovery linear advertising fell 11%. Scripps Networks contracted 11.1%. These are not rounding errors. They are the tollbooth converting to E-ZPass.

The problem is the debt.

They didn't just build streaming with cable's money — they borrowed against it. The bet: take out loans now, use cable revenue to make the payments, and let streaming profits take over before the math stops working. Warner Bros. Discovery is carrying $33.4 billion in debt. Paramount carries $15.5 billion. Gray carries $5.81 billion. Scripps carries $2.6 billion. Optimum wrote down $2.7 billion in asset value in a single quarter — a formal admission that the cable infrastructure it borrowed billions against is worth less than when it took out the loans.

The money leaving cable.

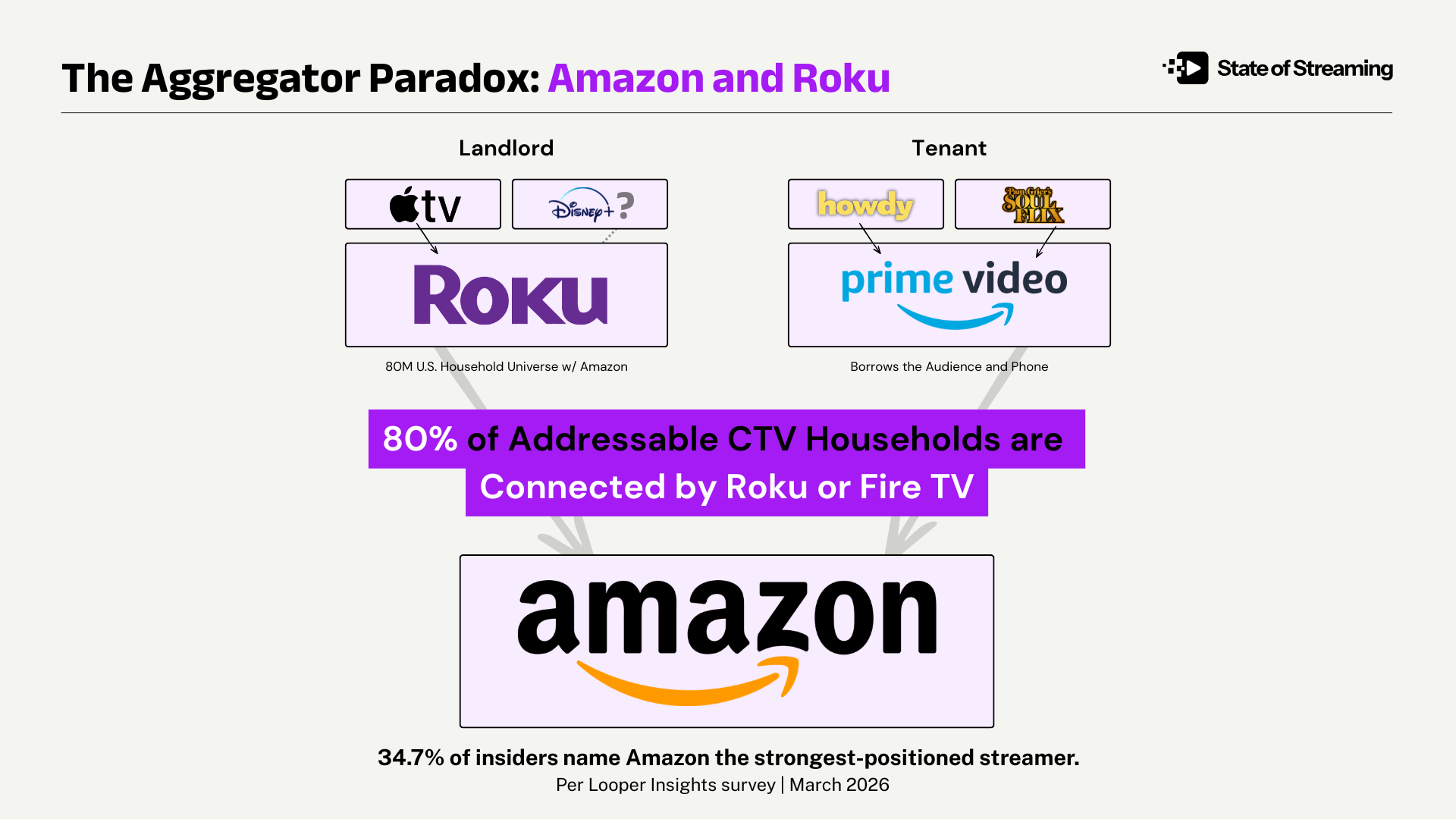

Amazon's advertising business cleared $70 billion in trailing revenue. Roku platform revenue grew 28%. The new tollbooths look like — distribution infrastructure with audience data, closed-loop measurement, and no legacy debt underneath them.

For the advertiser still treating this as a platform preference question, here is what the Q1 data actually says about your media plan.

Linear is the execution risk now.

A plan built on inventory from a company carrying $15 billion in debt is a plan built on a seller whose programming, rights renewals, and distribution agreements are all downstream of a debt service schedule. If Gray loses a retransmission negotiation, the inventory disappears mid-flight. Buying linear from a debt-distressed seller is not a value play. It is a liquidity subsidy. The advertiser is helping a media company make its loan payment.

Streaming infrastructure compounds.

Roku's advertising gross margin is 60.5%. The subscription side runs at 41.1%.

Amazon's ad business generates software-level returns.

Two platforms are reinvesting margin into better targeting, better measurement, and better inventory quality. Closed-loop measurement — knowing whether the person who saw the ad actually bought the product — is something linear never offered and never will.

The window to lock in streaming inventory at current rates is closing. As streaming profitability becomes consensus — and Q1 2026 confirmed it as consensus — the rate card will start to inch back up. Buyers who are still treating streaming as the experimental line item and linear as the guaranteed reach play are making a 2019 decision with 2026 money.

Read 'The Aggregator Paradox' Next

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.