Is Teads Running the DoubleClick Playbook?

Key Takeaways

The hire of TikTok's UK commercial architect and an aggressive $100 million adjusted EBITDA target for 2026 together signal a platform moving fast — for streaming executives and rights holders, the window to negotiate favorable terms is open now.

Teads' home screen CTV position — inventory sitting before content selection, not inside it — is structurally differentiated from the in-stream formats, making it a demand complement rather than a direct competitor for rights holder yield.

Independent supply path data puts Teads' CTV coverage at 14.8% of the premium programmatic market as of Q1 2026, against market leaders above 99% — streaming platforms evaluating Teads as a demand partner should price that gap into yield expectations until coverage closes.

The living room is the most contested advertising surface in 2026. Every major streaming platform, every device manufacturer, and every ad tech company with CTV ambitions is competing for the same household attention. Most of them are competing for inventory inside content. Teads is betting on the moment before content starts.

The Platform and the Bet

Teads Holding Co. is a year into its life as a merged entity — Outbrain's performance demand infrastructure combined with Teads' premium publisher supply relationships, rebranded and listed on the Nasdaq as $TEAD in February 2025.

The combined pitch looks like this:

A single platform running brand and performance campaigns across web, mobile, and connected television without leaving the open internet.

The structural playbook has precedent. Google acquired DoubleClick in 2008, kept the brand equity buyers already trusted, rebuilt the platform underneath it, and by the time the industry fully understood what had been built, the supply path was already the default. Teads is running a version of that playbook for itself. The difference is runway. Google had search revenue and a dominant ad server. Teads has a fiscal year.

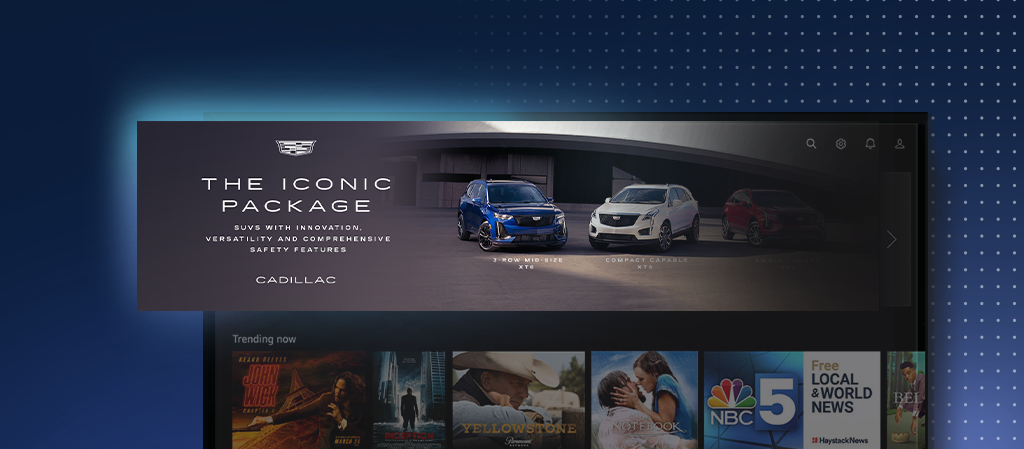

Teads crossed $100 million in annualized CTV revenue in Q4 2025, with 55% year-over-year growth. Its CTV position is built on home screen placements — the interface a viewer sees before selecting content — through OEM partnerships with major device manufacturers. The company claims access to more than 500 million addressable TV screens globally through those relationships.

Example of Teads CTV home screen placement.

That is a structurally different inventory position than the in-stream mid-roll formats most streaming platforms monetize today. The viewer has not yet chosen their content. Attention is still up for grabs. Inventory is limited. If the format proves out at scale, it sits adjacent to — not in competition with — the inventory streaming platforms are already selling.

The Signal in the Hire

Buyer conviction construction is Jit Shergill's specific skill — persuading major agency holding groups to allocate budget toward inventory formats that have no established buying playbook, using performance outcomes as the justification. Teads just hired him as UK Head of Sales. He built TikTok's UK commercial operation from early adoption to a multi-billion-pound agency business running that exact play.

The hire signals what Teads believes its 2026 constraint actually is. The OEM partnerships are signed. The platform architecture exists. What the home screen format still lacks is normalized agency demand — budget flowing toward it as a standard line item rather than a test. Shergill's job is to build that demand layer. For streaming platform executives watching where agency CTV budgets move next, that is worth tracking.

What This Means for Streaming

The home screen format deserves serious evaluation from rights holders and platform executives, not just media buyers. Teads reports CTV HomeScreen campaigns averaging approximately 5,300 Attention Per Mille (APM) — 173% higher than outstream video and 114% higher than YouTube. Those are self-reported figures from its Lumen Research attention measurement partnership and should be independently verified, but the format's structural attention advantage over contested in-stream inventory is real.

The streaming industry needs a scaled open internet CTV alternative to Amazon and Roku. Both operate closed ecosystems — controlled data, controlled auction, controlled measurement. A platform offering comparable household reach with transparent supply paths and open auction access changes the negotiating dynamic for every rights holder that has felt the weight of a walled garden deal.

The financial pressure sharpens the timeline. Teads entered 2026 with a Nasdaq compliance issue and a restructuring targeting $35 to $40 million in annualized savings. The 2026 guidance targets $100 million in adjusted EBITDA. Platforms under that kind of pressure move faster and deal sharper. For streaming executives willing to engage now, that is a negotiating window.

Learn about how Media Placement Value ($MPV) quantifies home screen placement value. Read this analysis next.

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.