Nielsen Delayed The Gauge. Here's What Media Buyers Should Do Before March 24.

Nielsen was supposed to release its February Gauge report next week. Instead, the company is pushing it to March 24 after clients who previewed the data asked for more context — not about what the numbers said, but about the methodology behind them.

The delay is tied to Nielsen's adoption of the ARF DASH TV Universe Study, a new household estimation framework developed through a partnership with a non-profit research center at the University of Chicago. The MRC accredited ARF DASH in February and Nielsen integrated it quickly. Clients say the integration moved faster than the explanation.

For media buyers heading into Upfront season, this isn't a reason to panic. Here's what's actually moving and what to do about it.

What Changed and Why It Matters for Planning

Nielsen confirmed that when it began standard monthly Gauge previews this week, some clients requested additional data around how DASH implementation affected February's results. The company is now aligning the Gauge release with the Media Distributor Gauge on March 24 to give the industry what it called "a smoother transition" and "a better holistic view of February viewing."

The early read on February was already notable. Super Bowl LX and the Winter Olympic Games drove significant broadcast and cable viewership on NBC and associated cable channels, including two Versant-owned networks that carried Olympic events after spinning out of NBCUniversal earlier this year. Traditional TV was poised to reclaim share from streaming for the month.

But here's the planning question: how much of that shift reflects actual audience behavior, and how much reflects a change in how total TV households are counted? Until Nielsen provides the supplementary DASH data, year-over-year comparisons against prior Gauge reports carry an asterisk. The MRC publicly questioned Nielsen's Big Data + Panel methodology last week, acknowledging that changes would be "disruptive to business processes of the marketplace."

A CIMM/4As study found that 43% of advertisers rated cross-platform measurement as a major or severe barrier, and Samba TV data showed 12 of the top 20 TV advertisers spent more money to reach fewer households in the same period. That's the environment heading into Upfront season. The buyers who bring independent data and a clear view of the landscape will negotiate from strength. Everyone else will be planning against someone else's math.

Netflix Enters the Upfront as a Different Company

In the span of 44 days this year, Netflix opened its ad inventory to audience targeting via Amazon DSP and Yahoo DSP, launched a proprietary Conversion API with early attribution results that outperformed benchmarks by more than 75%, consolidated product, engineering, and data under a single executive, acquired an AI production technology company, and walked away from an $83 billion WBD acquisition that would have multiplied its debt load five or six times over. The stock recovered 32% in eight trading days because the market saw what Netflix is building with the money it didn't spend.

For buyers, this means Netflix enters the 2026 Upfronts with programmatic access, behavioral targeting at scale, first-party attribution, short-form mobile inventory via its forthcoming vertical video feed, and a content pipeline spanning original production, global licensing, and live events in a single buy. As Jean Carucci, The Streaming Strategy Scholar emphasized on the State of Streaming podcast, "the first question every buyer should ask is whether you can activate your own first-party data on a platform or whether you're relying solely on native targeting tools". Netflix's DSP integrations now make that possible in ways that didn't exist even just a quarter ago.

The Paramount+ Merged Universe: What Buyers Should Be Modeling

On the other side of the M&A landscape, the Paramount and Warner Bros. Discovery merger creates a different kind of opportunity. As Carucci laid out in her Upfront framework, this combined entity offers something Netflix structurally cannot: massive reach across linear and streaming, endemic lifestyle content with high advertiser relevancy, and a live sports lineup that rounds out from March Madness to the NHL.

The trade-off is fragmentation. Two separate ad platforms, two sets of data requirements, potentially different creative specs, and a frequency capping problem that won't resolve until the planning systems unify mean that buyers going into these negotiations should be modeling duplicated reach explicitly and demanding clarity on how frequency will be managed across what will remain, for a while, parallel infrastructure.

But the content verticals matter. Reality, food, home, competition — this is sticky, high-affinity inventory where brand integrations are organic and CPG relevancy is native. Carucci's advice: shift from volume buying to venture buying. Lock tent-pole and live event inventory early, before the combined entity reprices it. And ask the integration question directly — what's the ad tech stack's capability for interactive, shoppable, and outcome-driven formats? A 30-second spot for brand awareness alone isn't the standard anymore.

The Unified Reach Play: Versant and Scripps Are Building It Now

Versant claimed 92% household reach in January 2026 by acquiring Free TV Networks for its pre-existing distribution relationships across broadcast and FAST platforms, then converting that footprint into deals with CBS and Sling Freestream within weeks.

E.W. Scripps is running a parallel thesis through ION. The network already carries more WNBA and NWSL games than any other national broadcaster, with dedicated studio shows for both leagues. The PWHL distribution deal extends a strategy Scripps has been building since 2023: women's sports can anchor a free, ad-supported national model. ION is becoming the destination for reaching women's sports audiences across linear and streaming — a unified footprint that doesn't require buyers to negotiate two separate deals to reach the same household.

Both companies share a structural insight: the platforms that control scaled reach spanning both systems now, while FAST inventory is still priced as remnant and the ad impression valley bottoms out, will have pricing power that competitors scrambling to build simply won't. The real estate is being claimed now.

Vertical Video: The Inventory Layer Nobody's Pricing Yet

Add one more variable to the Upfront planning equation. The entire streaming industry is converging on vertical video as a new ad surface, and the buyer who understands this inventory before it scales will have a first-mover advantage.

Disney+ launched Verts this week — a swipeable vertical video feed embedded in its mobile navigation bar, following ESPN's August rollout. Netflix has confirmed vertical video will anchor a full mobile app redesign later this year. Tubi has Scenes. Peacock is replacing its downloads button with a vertical video tab this summer, powered by an AI system that can slice over 5,000 hours of Bravo footage into more than 600 billion potential viewing combinations. Peacock is also using AI to crop and reformat live NBA action into vertical video in real time.

According to NBCU during the 2026 Winter Olympics, 20% of viewers who watched vertical highlight clips navigated directly to the full live stream.

The pitch to advertisers is compelling: social-style engagement rates, streaming-grade brand safety, first-party targeting, full-screen sound-on by default. If this inventory materializes at scale, it won't just compete with TikTok and YouTube Shorts — it will reprice them entirely. Disney's Brand Impact Metric, announced alongside Verts at CES, is designed to bridge brand and performance measurement across exactly these cross-format campaigns which indicates they're building the measurement infrastructure for inventory that doesn't exist at scale yet.

For buyers, the action item is straightforward: ask every platform in your Upfront conversations what their vertical video roadmap looks like, what the ad load model will be, and whether your first-party data activates against that inventory. This surface is being built right now. The pricing will never be lower than it is in the first cycle.

The Real Question Heading into March 24

Nielsen says the DASH framework "more accurately reflects the TV landscape." That may well be true. But accuracy and adoption aren't the same thing — and commitments won't wait for the industry to agree on which version of the truth to trade on.

The measurement currency is in flux. The largest platforms are building proprietary attribution systems that bypass it entirely. New ad surfaces are emerging that the current measurement infrastructure wasn't designed to capture. And the companies spanning linear and streaming simultaneously are building unified reach before the market prices it correctly.

The Gauge will land on March 24. In the meantime, we got started on The Grid™️in an effort to establish an Open Source, directional methodology that can be used to compare streaming apps as television measurement will continue to evolve.

We have 295 more apps to add and welcome your feedback along the way.

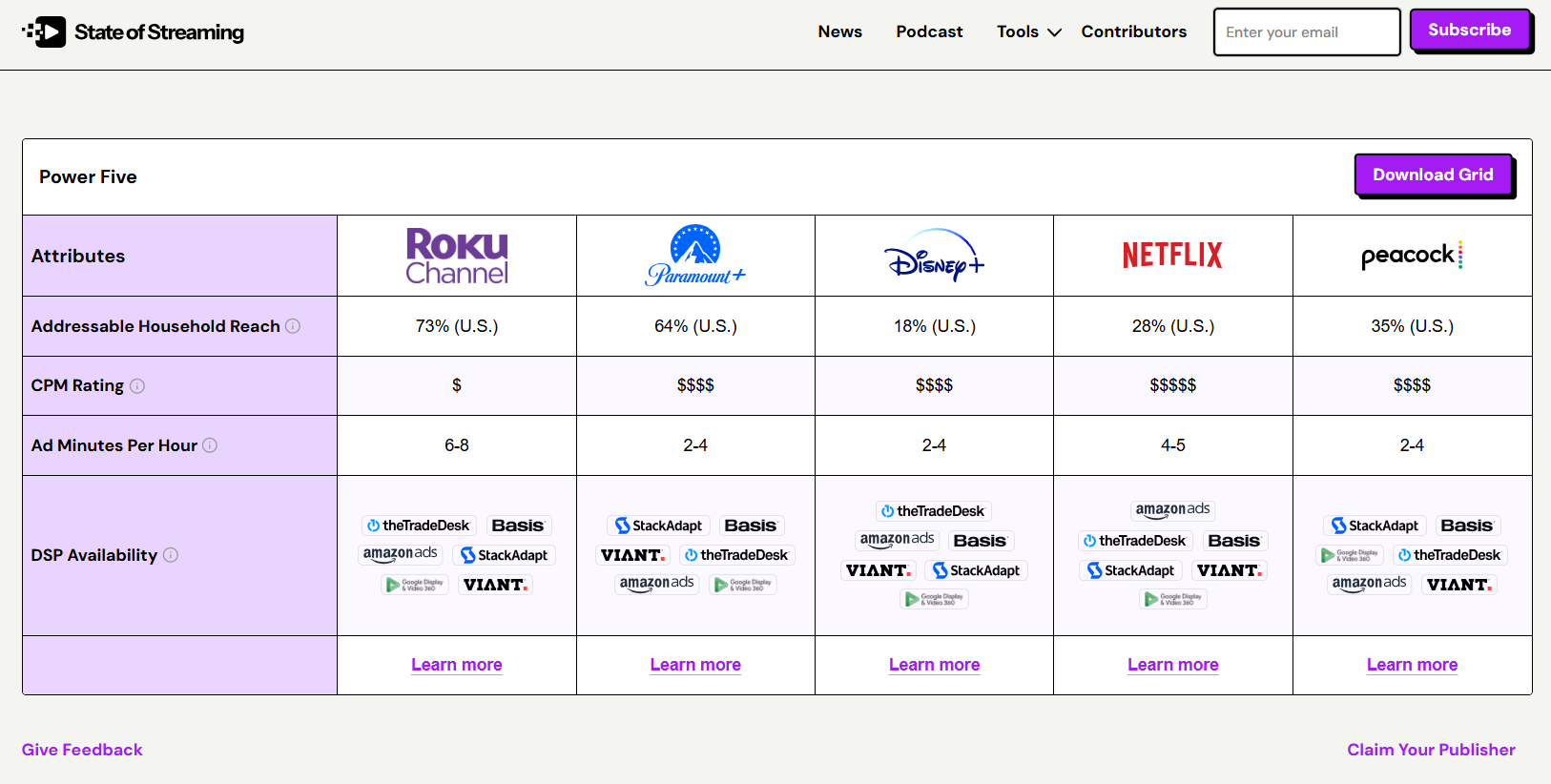

How the Addressable Household Reach methodology works:

Peacock has 44M U.S. Households. Which means that of the 123,873,624 internet connected U.S. Census Households, Peacock has an estimated 35% Addressable Household Reach.

Get the SOS. Brief

The sharpest streaming intelligence, delivered to your inbox.